Tackle Your Student Loans

For many recent college graduates, your first post-grad summer is kind of like a honeymoon. You’re still riding the high from graduating and enjoying your first tastes of “adulting,” but perhaps a “lite version” of adulting, with fewer responsibilities. Six months after their ceremony, college grads all across the country get the wakeup call they never signed up for. Student loans. Who gave Sallie Mae our numbers, anyway?

Whether state or federal, subsidized or unsubsidized, student loans are daunting. Oftentimes, when faced with a situation as overwhelming as paying off your student loans, our initial reaction is to avoid it altogether. Take it from us, you do not want to ignore your student loans. The consequences of not paying your loans can be costly and they tend to follow you around for years. Bad credit, rising interest loans, and falling behind on payments can send you into a downward spiral of greater debt and fewer economic opportunities.

Don’t sweat it too much though! While they may appear overwhelming, student loans are nothing to fear! You can manage them on your own! Follow our advice for taking control of student loan debt on your own, no super-rich families or inheritances required.

Shine a Light on Your Student Loans

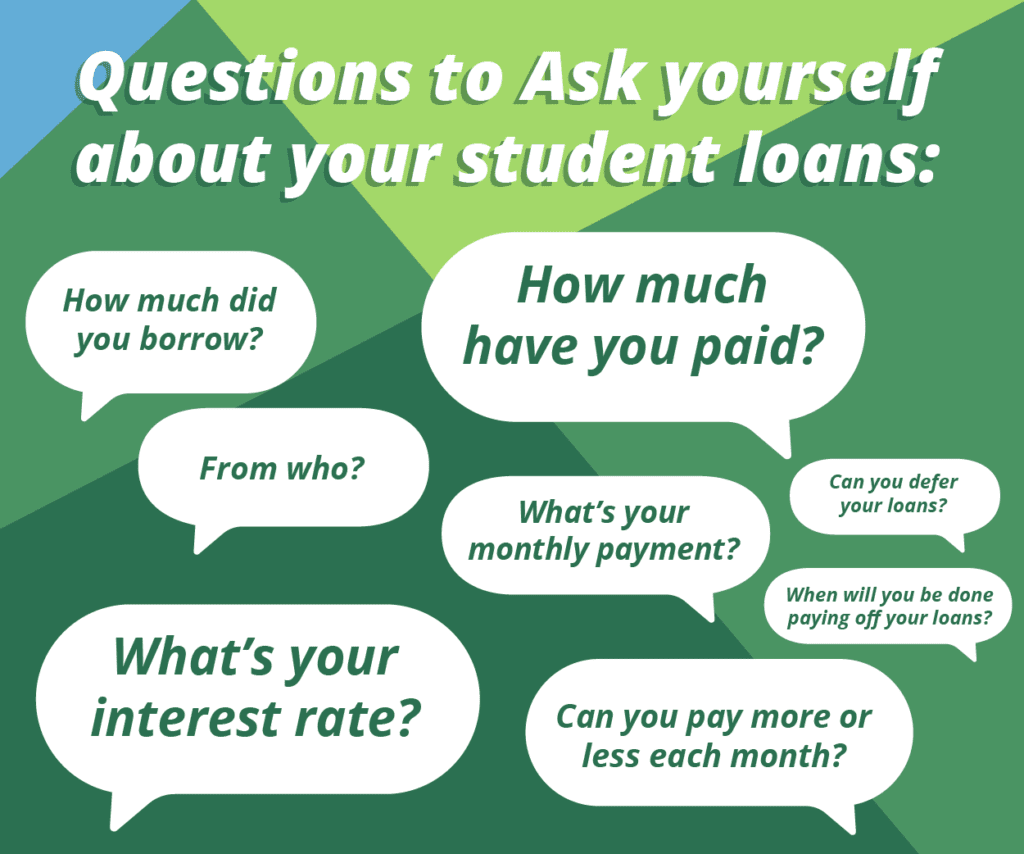

The first, and most critical, step to taking control of your student loans, is to shine a light on them. You have to be intimately aware of your standing. Ask yourself the following questions, and if you can’t answer them, be prepared to do some digging into your accounts.

You can check the National Student Loan Data System (NSLDS) to find a full list of federal student loans in your name. You can also review your credit report to verify that it lists your NSLDS accounts accurately. Your credit report should also list your private student loan amounts, as well as any federal student loans you may have taken out.

Once you know how much you owe, it’s time to own your debt. Take it for what it is, the good, the bad, the ugly. Take a deep breath. Trust that even a seemingly giant student loan bill can be controlled — it’s just a question of finding a solution that fits your situation.

Set Your Sights on Your Student Loans

Are your student loans stressing you out? If you’re human, probably. Don’t let that overwhelm you though. Feeling stress, anxiety and even anger are all totally normal. Fighting these emotions, in regards to both your student loans and life in general, will not do you any good. It may be easier said than done, but do your best to own those emotions, as opposed to trying to avoid them or fight them. Getting angry with yourself for being anxious doesn’t make you less anxious, it just makes you anxious and angry.

Use whatever stress, anxiety, anger, sadness, or other emotion fuel you as you set your sights on your student loans. Imagine how accomplished (and relieved) you’ll feel once you pay your last bill, and remember, you can and you will pay your last bill!

Consider ways to relieve your stress as you tackle repayment.

Recognize the Progress You Make

For most of us, student loans are a 10, 15, even 20-year commitment. As a 22-year-old entering the “real world” for the first time, that probably seems like a lifetime (it doesn’t feel like one though. Again, you’ll have to trust us on this). You can easily slip into feeling overwhelmed when you think about your student loans as “lifetime commitment,” so try to break it up into manageable chunks and be sure to celebrate the progress you make.

Start by setting reasonable goals. Maybe every $100 or $1,000, or whatever works for you really, you celebrate a bit. Whether it’s grabbing a nicer dinner than what you normally eat, throwing some confetti, or just sharing your progress with someone close to you, don’t let any milestones pass you by.

Recognizing the progress you make in paying off your student loans makes them more attainable. Scaling a few small mountains is much easier than summiting Everest. Be gentle with yourself, and pat yourself on the back every once in a while. You’ve earned it.

Set a Budget. Stick To It

This is the hardest part. As a recent grad facing student loans, you’re also probably making “real money” for one of the first times. With your fancy new job comes a fancy new salary, and you may be tempted to spend it all. Fight the urge.

While treating yourself from time to time is fine (even encouraged!), you’ll need to be responsible and diligent about your budget. Set aside money for your student loans and other bills each month before you spend any extra money on fun splurges.

It may seem like obvious advice, but again, take it from us. So many young adults slip into even more debt after graduating due to the temptations and freedoms of adulthood and having a more disposable income. Training yourself to be diligent from the start will only make it easier for you to pay off your student loans.

Explore a Side Hustle to Help Offset Your Student Loans.

Have you ever heard the phrase “if you’re good at something, never do it for free?” If not, well, you have now! Find something you’re passionate about and explore ways to turn it into your “side hustle.”

With the rise of Etsy and other online retailers, the possibilities for your next side hustle are endless. As Cardi B once said, “I don’t do nothing for free you know I got to charge.” If you can make some extra cash from something, why not?

Look Into Tax Deductions Or Other Credits Available to You

When working on your tax returns, keep in mind you might be eligible for student loan interest deductions. While you must meet some basic requirements in order to be eligible, this could easily deduct up to $2,500 on your taxes yearly, helping you to keep more of your money and put it toward paying off debt.

The student loan interest deduction It is one of several tax breaks available to students and their parents to help pay for higher education, so be sure to do some research and see what other breaks you can apply to!

Make Extra Payments to Your Student Loans

The most intimidating (and frustrating) part of paying back your student loans is the accumulating interest. Over time, the amount you owe will continue to accumulate interest, just adding to your total balance. Interest is calculated as a percentage of the total sum you still owe, so the larger your loan, the more interest you’ll have to pay.

It’s kind of a domino effect. It can be hard to see the light at the end of the tunnel. Many students find themselves making payments every single month, and not even covering the accrued interest, meaning their balance never drops.

Is hard as it may be, whenever you come into an extra sum of money, consider using it to pay off your student loans. Birthdays, holidays, and year-end bonuses can be great additional incomes to help you get ahead of your loans, and reduce your balance before your interest gets too overwhelming. By following this strategy, you could be debt-free years ahead of schedule.

We’re Here to Help

While we can’t pay your loans off for you, Addison Group can help you find your dream job. Contact an Addison Group professional today to take the next step in your career, land that sweet new gig, and maybe even add a few dollars to your paycheck so you can pay off your loans faster.